Note

Go to the end to download the full example code.

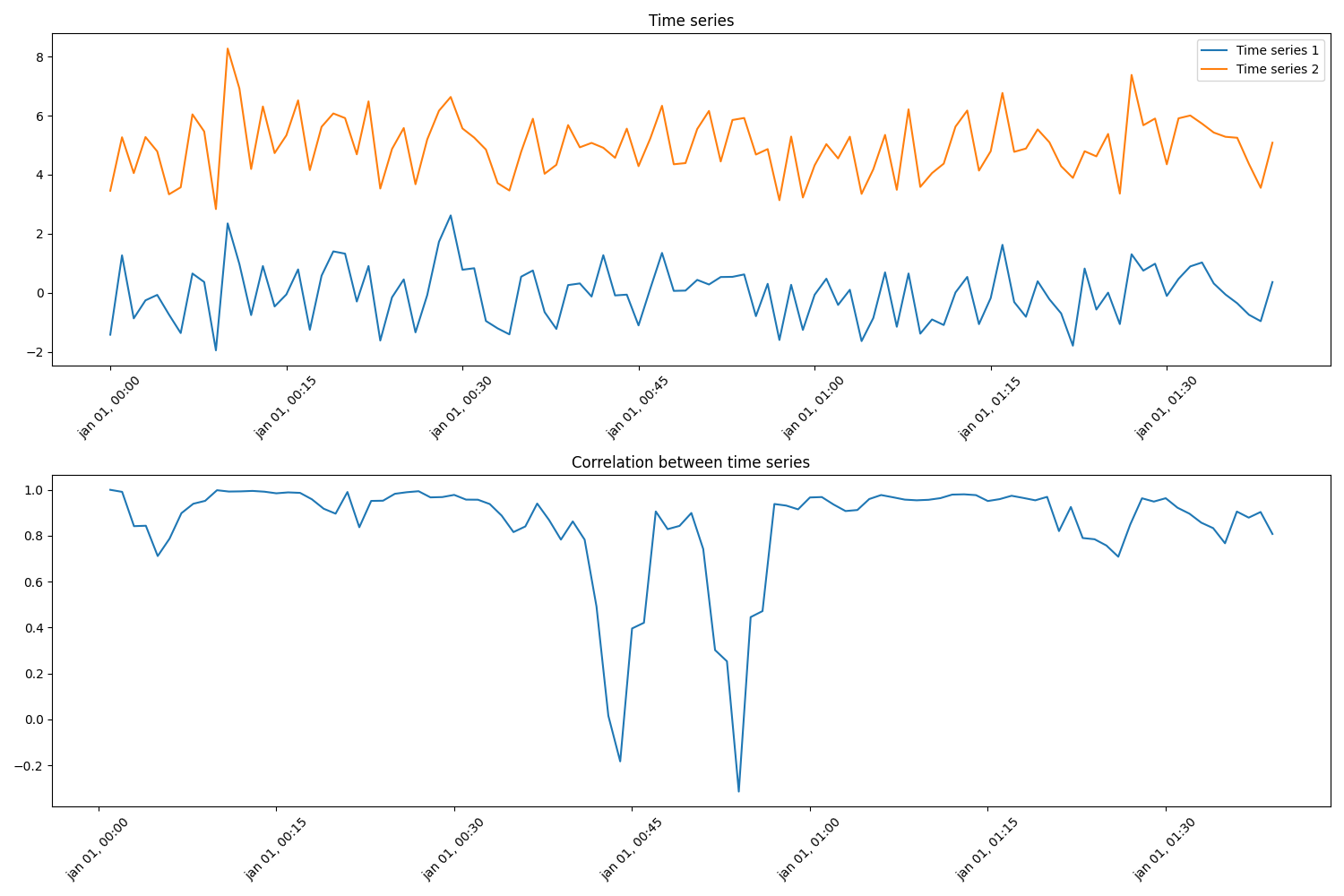

Pearson correlation

This example calculates the rolling pearson correlation coefficient between two synthetic timeseries.

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from matplotlib.dates import DateFormatter

from indsl.statistics.correlation import pearson_correlation

# generate the data

rng = np.random.default_rng(12345)

num_datapoints = 100

y1 = rng.standard_normal(num_datapoints)

y2 = y1.copy() # create data2 from data1

y2 += 5 # add deviation

y2 += rng.standard_normal(num_datapoints) * 0.5 # add noise

index = pd.date_range(start="1970", periods=num_datapoints, freq="1min")

data1, data2 = pd.Series(y1, index=index), pd.Series(y2, index=index)

# calculate the rolling pearson correlation

corr = pearson_correlation(data1, data2, time_window=pd.Timedelta(minutes=5), min_periods=1)

# Plot the two time series and the correlation between them

fig, ax = plt.subplots(2, 1, figsize=[15, 10])

ax[0].plot(

data1,

label="Time series 1",

)

ax[0].plot(data2, label="Time series 2")

ax[1].plot(corr, label="Rolling pearson correlation")

ax[0].set_title("Time series")

ax[1].set_title("Correlation between time series")

_ = ax[0].legend(loc="best")

# Formatting

myFmt = DateFormatter("%b %d, %H:%M")

for ax_ in ax:

ax_.xaxis.set_major_formatter(myFmt)

ax_.xaxis.set_major_formatter(DateFormatter("%b %d, %H:%M"))

_ = plt.setp(ax_.get_xticklabels(), rotation=45)

plt.tight_layout()

plt.show()

Total running time of the script: (0 minutes 0.267 seconds)